43+

160+

130+

9500+

14+

10+

Established in 1980, D. Zavos Group has created a revolutionary concept in the Cyprus property and development industry, with a holistic offering of exceptional value and solid investment opportunities, as well as comfort and services synonymous with a 5-star hotel.

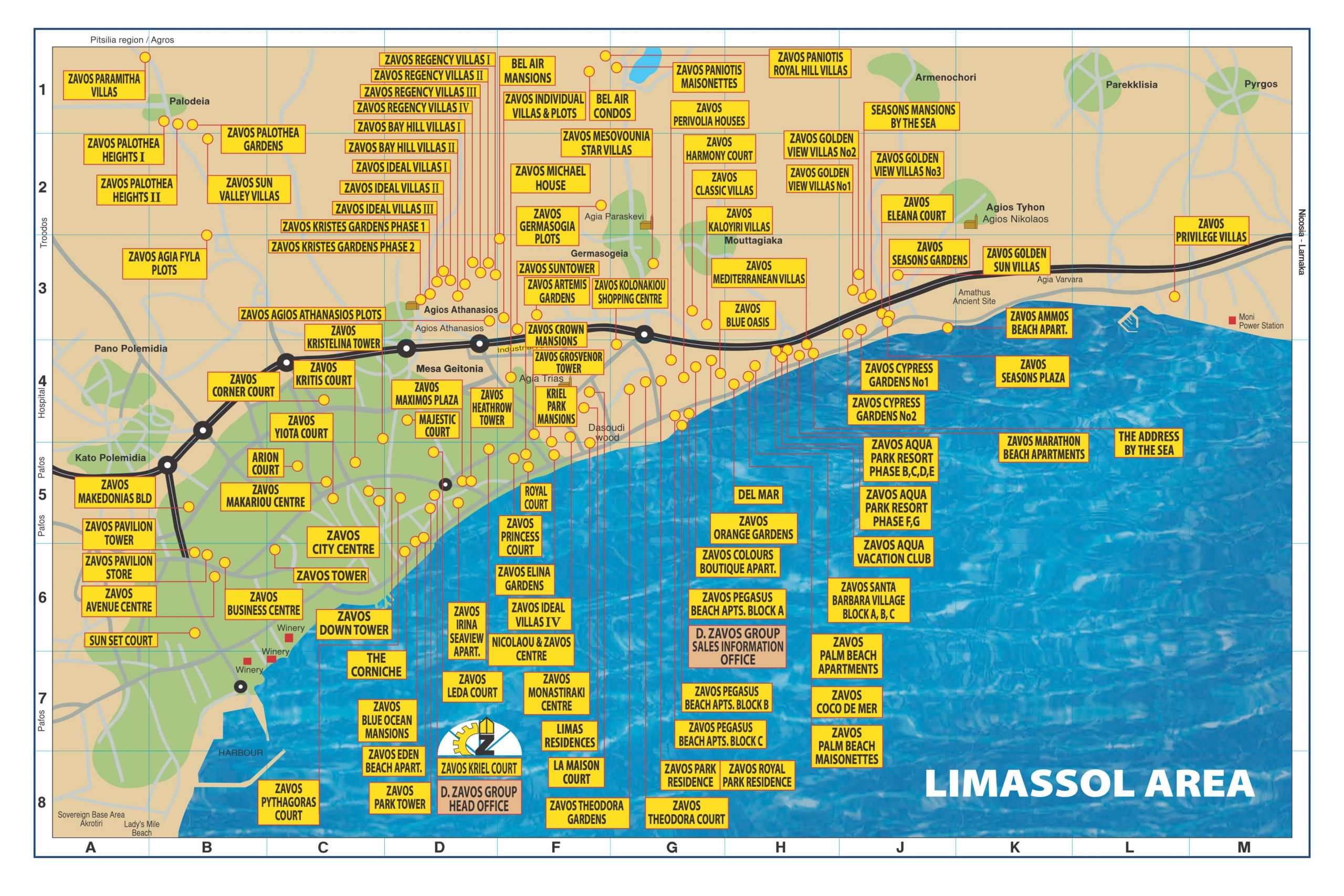

Based in Limassol, D. Zavos Group offers clients a variety of cutting-edge properties in prime locations all across Cyprus. These include luxury villas, apartments, and residences, available to rent or buy. The Group also possesses a large portfolio of commercial properties that can be rented out to companies for investment purposes. Currently, D. Zavos Group boasts more than 160 Commercial and Residential projects in Cyprus, of which 130 have been issued with separate title deeds.

Learn MoreD. Zavos Group is always a step ahead with new residential property developments in the most prestigious and sought-after areas of Limassol. From eye-catching high-rise developments with sea view apartments to luxury villas, D. Zavos offers its clients a wide range of property portfolios to choose from.

View PropertiesLuxury completed properties situated in the cosmopolitan city of Limassol, Cyprus, D. Zavos Group delivers contemporary designs for comfortable modern living. Exceptional property developments of two and three-bedroom apartments, maisonettes and homes for your family.

View PropertiesD. Zavos Group offers a wide portfolio of ready apartments and villas within easy reach of all local amenities and in prime locations of Limassol city.

View PropertiesD. Zavos offers elegant buildings for commercial and office use in Cyprus. Whether situated on the bustling seafront promenade, with sweeping views of Limassol’s coastline or at the heart of vital commercial roads, D. Zavos covers all needs and preferences.

View Properties